September 25, 202511 min read

Equity Advisor Duties: A Simple Guide for Indian Founders

By Abhishek Bhanushali

Finance Advice

As a founder, you already know that money is the fuel that keeps your business running. But here's what might surprise you: despite SMEs contributing nearly 30% to India's GDP and employing over 110 million people, accessing that fuel remains one of the biggest headaches for business owners like you.

The numbers tell a stark story. A 2024 SIDBI report reveals that Indian MSMEs face a credit gap of around ₹30 lakh crore. That's not just a statistic—it represents countless sleepless nights for founders worrying about cash flow, missed growth opportunities, and the constant stress of keeping operations afloat.

If you've ever felt frustrated by bank rejections, overwhelmed by paperwork, or stuck in a cash flow crunch, you're not alone. Let's break down why funding feels like an uphill battle and, more importantly, what you can do about it.

You have a solid business idea, paying customers, and growth potential, yet banks are reluctant to treat your loan application. As a founder, you're dealing with challenges that go beyond simple loan rejections. These are systemic issues that affect how you run your business every single day.

Here's why this happens and what it means for your day-to-day reality:

Now that we've acknowledged these pain points, let's dig deeper into the new solutions designed specifically for the challenges affecting your business right now.

At S45, we've learned that the most successful founders aren't necessarily the ones who know everything, but those who know when and where to get the right guidance.

The traditional lending system wasn't built for businesses like yours, but that's changing fast. Let's look at the solutions that are already helping founders overcome these challenges.

The government has launched several initiatives to bridge the financing gap for MSMEs, helping businesses scale and grow sustainably:

1. Credit

2. Technology

3. Market opportunities

These initiatives are crucial for empowering businesses to expand and thrive in competitive markets.

The most exciting changes are coming from fintech companies that understand your challenges because they were built specifically to solve them.

1. Provide access to working capital immediately when you deliver goods and services. The lender gets paid when your customer pays.

2. Eliminate the need for physical collateral, ensuring more inclusive financing options.

These aren't future concepts. They're available now and helping founders just like you solve their immediate cash flow challenges.

As the need for specialized financing grows, these emerging solutions offer fresh opportunities:

1. Women-led MSMEs face a $158 billion credit gap.

2. Microloans and women-focused credit lines are being introduced to address this disparity.

1. Focuses on supporting MSMEs adopting eco-friendly practices.

2. A key area for future growth, providing financing for businesses committed to sustainability.

These solutions are paving the way for more inclusive and sustainable financing opportunities for MSMEs.

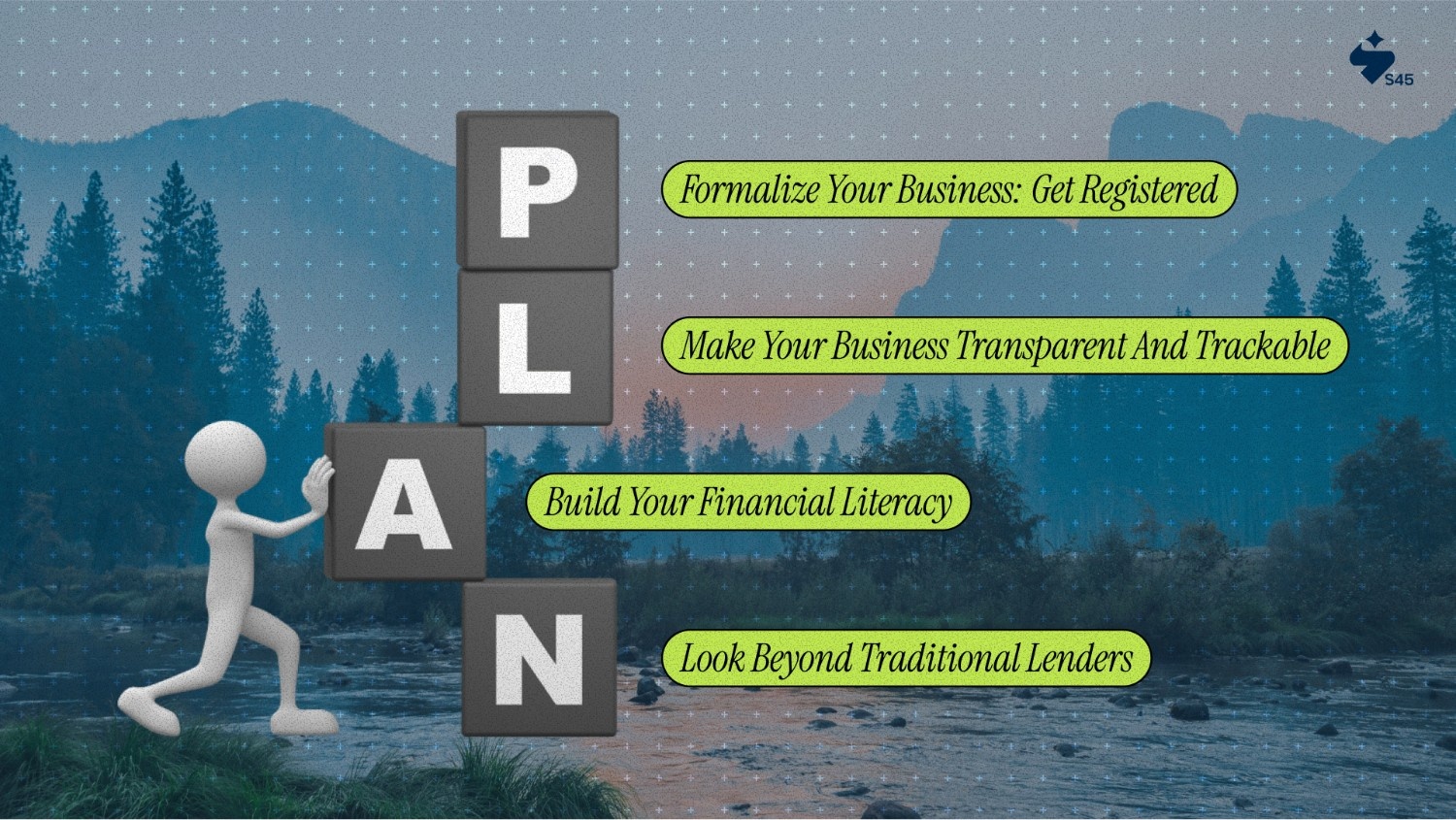

But knowing about these solutions is just the first step. Let's talk about what you can actually do starting tomorrow.

Reading about solutions is one thing, but implementing them is what will actually change your situation. Here's your practical roadmap for improving your access to funding.

At this point, you might be thinking: "This all sounds good, but how do I actually execute this while running my business?" This is where having the right partnership becomes crucial.

Securing capital is just the first step. For a business to achieve sustainable growth, you need more than just a financial injection. You need a partner who understands your vision and provides the strategic expertise to help you scale.

This is where the S45 can help you thrive.

If you're ready to move beyond the frustrations of traditional financing and partner with people who are committed to your long-term success, let's connect!

The government has introduced several tax benefits for MSMEs. Businesses with annual revenue under ₹50 crores now pay a reduced tax rate of 22%. The ceiling for presumptive taxation has increased, easing the tax burden. The government has also raised the threshold for GST registration and offered a 15% investment allowance on new plant, machinery, and equipment to encourage growth.

To apply for an MSME loan, lenders typically ask for recent passport-size photographs, proof of business address (rent agreement or utility bill), bank statements from the last six months, and Income Tax Returns (ITR). A certificate of business establishment and KYC documents like PAN or Aadhaar cards are also required for identity verification.

PMMY provides micro-credit in four categories:

Indian MSMEs face challenges such as poor infrastructure, including inadequate transportation and inconsistent electricity supply, which hinder productivity. They also struggle with fierce competition from larger companies and limited resources for branding and marketing, making it difficult to stand out in the market.

Discover more insights on similar topics

Get startup insights and connect with our community