September 25, 202511 min read

Equity Advisor Duties: A Simple Guide for Indian Founders

By Abhishek Bhanushali

Finance Advice

Small and medium enterprises form the backbone of India’s economy, contributing nearly 30% to GDP and employing over 110 million people as of 2024. Yet many units face persistent hurdles: outdated machinery limits productivity, compliance gaps restrict market access, and delayed payments from large buyers strain cash flow.

Competing with bigger players or meeting export standards often feels out of reach because the cost of upgrading technology remains prohibitive.

The Credit-Linked Capital Subsidy Scheme (CLCSS) was introduced to close this gap by reducing the financial burden of technology adoption, giving Indian MSMEs a viable pathway to modernization and long-term stability.

This blog explains how CLCSS works, its objectives, eligibility, application process, and how it connects with the persistent challenge of delayed payments faced by MSMEs.

The Credit-Linked Capital Subsidy Scheme (CLCSS) is designed to offset the high cost of plant and machinery upgrades, making modernization accessible for micro, small, and medium enterprises.

By subsidizing institutional loans, the scheme reduces entry barriers to technology that directly improves output, compliance, and competitiveness.

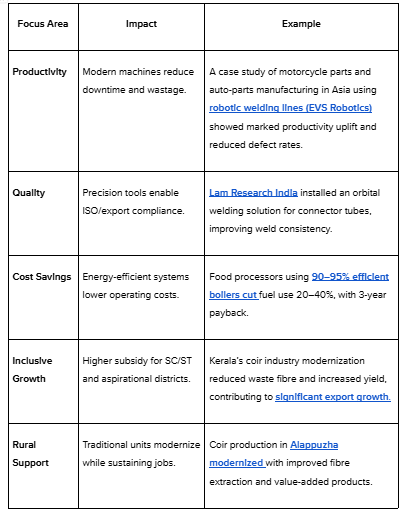

Beyond the direct financial support, CLCSS also plays a pivotal role in improving the broader operational landscape of MSMEs. Let's explore these impacts in detail.

CLCSS addresses the three bottlenecks that hold MSMEs back: productivity gaps, inconsistent quality, and limited access to modern markets. Let us further see how:

The government targets raising the MSME sector’s GDP contribution from 29% to 50% over the next decade, and CLCSS is positioned as a key lever in this transition

For founders, adopting schemes like CLCSS is only one part of the growth journey. Scaling a business requires not just capital relief but also guidance on compliance, strategy, and sustainable expansion.

This is where s45club positions itself, walking alongside MSME leaders, combining financial expertise with long-term growth support, and building a community focused on legacy and innovation.

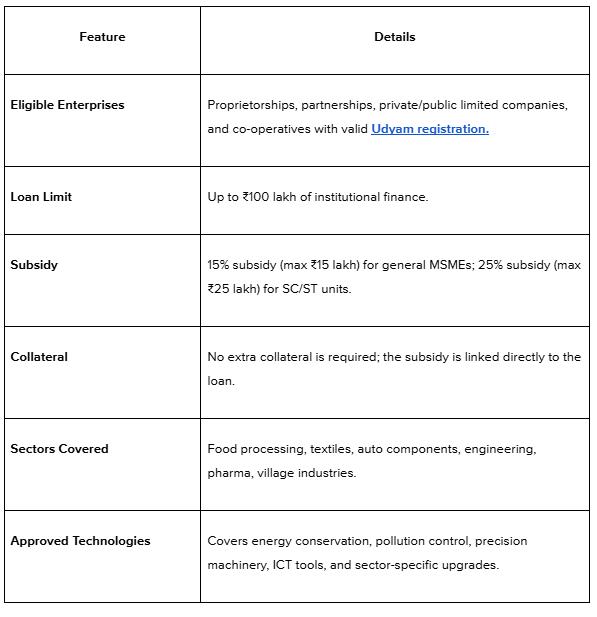

The design of CLCSS ensures broad applicability across ownership structures and sectors, while maintaining strict caps on subsidy limits.

Example: An auto-component MSME investing ₹80 lakh in robotic welding lines would qualify for a subsidy of ₹12 lakh under the general scheme, reducing the effective loan burden to ₹68 lakh.

The CLCSS application is routed through a single digital portal, reducing paperwork and delays. MSMEs apply online, their bank verifies the request, and nodal agencies release the subsidy once approved.

The system ensures transparency and allows applicants to monitor progress in real time.

Steps to Apply:

Processing Time: 6–8 weeks, depending on document accuracy and bank response.Tracking: Status can be checked anytime on the portal.

Tip: Verify machinery against the approved technology list before applying; ineligible equipment is a common reason for rejection.

While CLCSS helps improve operational capacity, it doesn’t address the ongoing challenge of delayed payments. Let’s dive into how delayed payments continue to impact cash flow and sustainability for MSMEs.

Upgrading machinery under CLCSS improves output and competitiveness, but these gains are undermined if delayed payments block cash flow.

Even well-equipped enterprises cannot sustain operations without timely receivables, making payment discipline as critical as modernization.

To address this, India has introduced legal safeguards and reporting systems:

India has implemented a robust set of legal safeguards to ensure timely payments to MSMEs. These frameworks are designed to protect MSMEs from delayed payments and ensure financial discipline from buyers:

Despite the legal frameworks in place, delayed payments remain a significant challenge for MSMEs. The scale of the issue continues to grow, underscoring the need for more effective enforcement and timely payment practices:

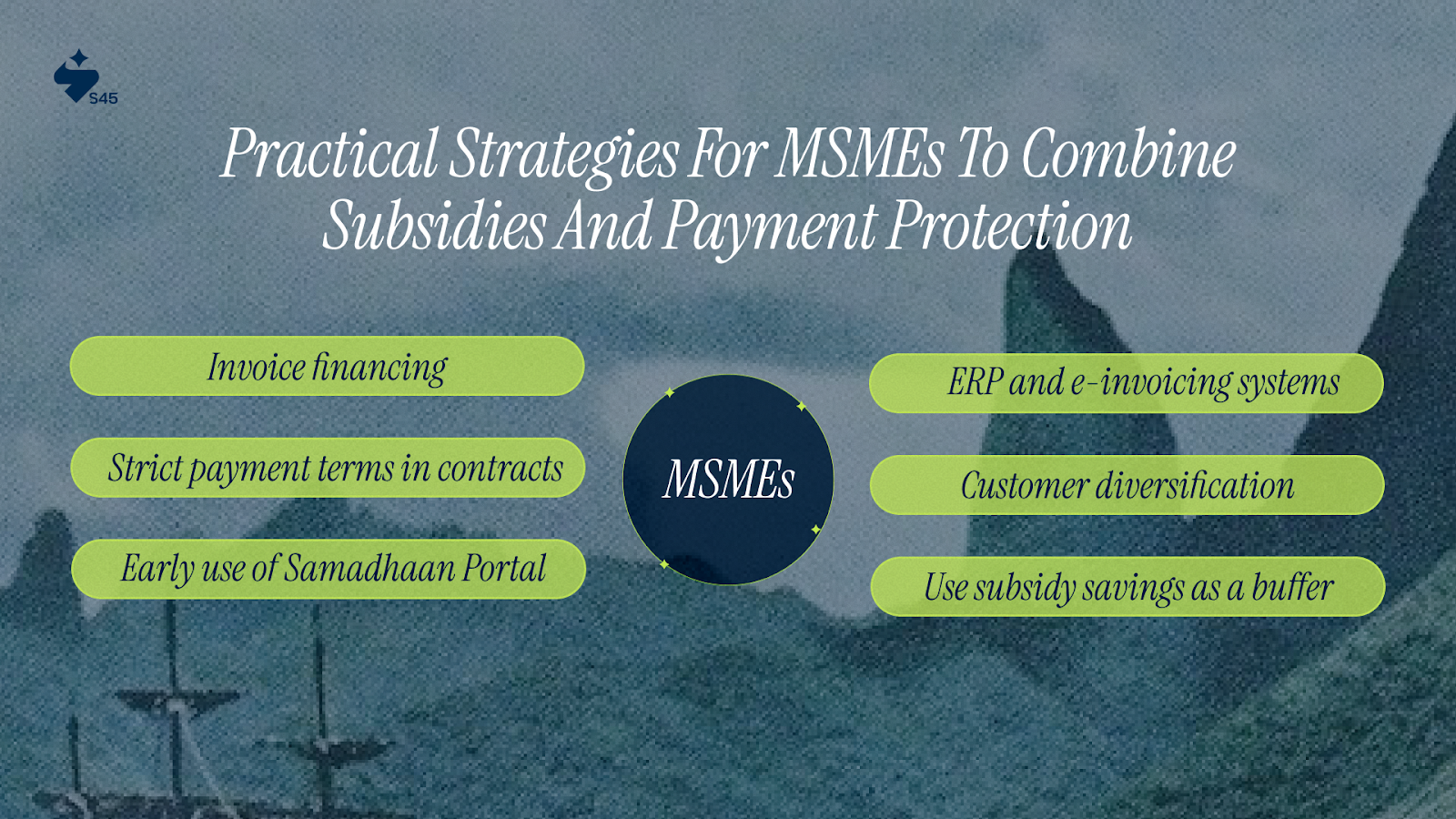

Now that we’ve established the significance of delayed payments, let’s examine practical strategies MSMEs can adopt to combine the benefits of CLCSS with proactive measures for managing cash flow.

Modernization through CLCSS improves efficiency, but delayed payments can still disrupt cash flow and blunt these gains.

The subsidy reduces upfront financial pressure, giving MSMEs some cushion, yet lasting stability requires a mix of subsidy benefits, financial tools, and legal safeguards.

Combining these approaches helps enterprises keep operations steady even when receivables are delayed.

Receivables often remain stuck with buyers for 60–90 days or longer. Factoring and platforms like TReDS enable MSMEs to sell approved invoices to banks or NBFCs and receive immediate cash. This helps maintain steady cash flow without waiting for buyers to release payments.

Example: A component supplier on TReDS sells invoices worth ₹25 lakh to a bank and receives funds within 3 days, avoiding a liquidity crunch.

Contracts and purchase orders should clearly include the 45-day payment mandate under the MSMED Act. Adding penalty clauses or interest terms discourages buyers from pushing payments indefinitely. Written terms give MSMEs firmer ground if disputes escalate.

Many businesses wait months before filing claims, which weakens their position. Filing cases as soon as payments cross due dates creates early pressure on buyers and brings the case under the notice of authorities. This can also help track repeat offenders when dealing with government or PSU buyers.

Manual tracking of invoices leads to errors and missed follow-ups. ERP systems integrated with GST e-invoicing provide automated reminders, clear receivable records, and digital proof of dues. This improves internal cash planning and strengthens any legal claim.

Example: A mid-sized food processor integrates ERP with GST e-invoicing and reduces overdue invoices by 30% within one year.

Dependence on a few buyers exposes MSMEs to high risk when payments are delayed. By balancing between large clients, regional buyers, and exports, units reduce the impact of any single delayed payment.

Example: A textile unit in Surat works with both exporters and domestic wholesalers, ensuring steady turnover even when export payments slow down.

The subsidy from CLCSS reduces the effective loan burden. A portion of this saving can be earmarked as a reserve fund.

This buffer allows enterprises to meet salary, raw material, and utility expenses during payment delays without resorting to costly short-term borrowing.

For MSME founders, raising capital is rarely the only challenge. The bigger hurdle is knowing when to raise, how much to raise, and what it means for ownership and long-term stability.

s45club was created to guide businesses through these decisions, combining access to capital with deep equity advisory designed for India’s growth-focused enterprises.

The Credit-Linked Capital Subsidy Scheme has given MSMEs a practical way to upgrade technology without taking on unsustainable debt. Better machinery raises productivity, improves compliance, and expands access to markets. Yet modernization alone cannot sustain growth if liquidity remains locked in overdue receivables.

Payment discipline under the MSMED Act and Section 43B(h), combined with financial tools like TReDS and invoice factoring, is just as critical.

Looking to learn from peers who’ve scaled with strategic capital? Join the s45club community to share experiences, compare playbooks, and grow alongside other founders.

A: No, MSMEs can apply for the CLCSS subsidy once per machinery upgrade. If additional upgrades are needed, they must seek separate funding through other schemes or financial institutions.

A: CLCSS supports MSMEs in adopting energy-efficient technologies, such as energy-saving boilers and machinery, which help reduce operating costs. These upgrades are critical for long-term sustainability and cost reduction in operations.

A: Yes, CLCSS covers over 750 approved technologies across 51 sectors, including food processing, textiles, engineering, and rural industries like coir and khadi, ensuring broad applicability for MSMEs in various industries.

A: No, the subsidy from CLCSS is strictly for machinery and technology upgrades. It cannot be used directly for working capital. However, the improved productivity from the upgrades can indirectly free up cash flow.

A: Yes, the scheme is designed to assist both small and medium-sized enterprises (SMEs) in India, offering the same subsidy rates for both categories, provided they meet the eligibility criteria and loan requirements.

Discover more insights on similar topics

Get startup insights and connect with our community