September 25, 202511 min read

Equity Advisor Duties: A Simple Guide for Indian Founders

By Abhishek Bhanushali

Finance Advice

Bank loans rarely work at the speed your business needs. You’ve probably hit that wall too: long paperwork, collateral you don’t have, or a rejection with no clear reason. Meanwhile, others around you are raising funds through revenue-based financing, leasing, or community capital, and scaling without the baggage.

That’s the shift happening in SME alternative financing, and it’s not just buzz. India’s alternative finance market is set to double, while MSMEs stare at a $220 billion credit gap.

If you’re building something and tired of dead ends, this article walks you through real funding models that match your stage, burn, and control goals. You’ll find what works, what doesn’t, and what to watch for.

Only 11% of Indian MSMEs get formal credit. The rest make do with personal funds, delayed receivables, or informal lenders. If you’ve tried raising through banks, you know the drill: slow approvals, collateral demands, and rigid terms that don’t match your stage.

Here’s what pushes many founders to look elsewhere:

Whether you’re planning a key hire, a product launch, or an inventory ramp-up, traditional lenders rarely move at the pace you need. Weeks go by chasing approvals, only to be asked for more documents.

By the time funds come through, if they do, the window of opportunity has often passed.

If you run a service-based or online-first business, chances are you don’t have property or machinery to pledge. Banks still weigh physical collateral heavily, regardless of how steady your cash flow or how fast your customer base is growing.

Long receivable cycles are common, especially in B2B. But traditional lenders rarely offer solutions tailored to that gap. You’re expected to manage repayments monthly, even when your own payments are due every 45 to 60 days.

Schemes like CGTMSE and SIDBI technically support collateral-free lending. But in practice:

This is where SME alternative financing steps in, not as a fallback, but as a model that’s actually built for how businesses grow today.

Exploring SME alternative financing can feel overwhelming. Different models, different trade-offs, and each comes with its own learning curve. Most founders know what capital they need, but not always which structure fits best at their stage. That’s where guidance matters as much as access.

Platforms like S45club have emerged to help bridge this gap. Instead of just pointing you to money, they help you step back and ask: What kind of capital do I actually need right now, and how does it shape the business I want to build?

Here’s how founders use equity advisory platforms like S45 to avoid costly mistakes:

Instead of chasing capital reactively, you start aligning it with your story, your stage, and your future rounds. That’s the real power of alternative financing for SMEs when it’s done with strategy.

Not all capital serves the same purpose, and not every funding model fits your stage, cash flow pattern, or growth plan. The key is to stop chasing what’s available and start choosing what’s right. Let’s break down some alternative financing models:

Ideal for growth-oriented SMEs seeking strategic backing through a potential ownership dilution. Works best when you’re chasing scale, not just survival.

Equity financing brings not just money, but networks, mentors, and credibility.

Best for SMEs that want to retain ownership but need liquidity for operations, expansion, or short-term working capital.

Debt lets you scale without losing ownership—but repayment discipline is key.

If your receivables or inventory are locked up, these financing tools help you unlock working capital without waiting for long credit cycles.

This category is scaling fast in India as RBI-backed platforms (like TReDS) gain traction in 2025.

For SMEs in priority sectors, government-backed schemes and grants reduce financing costs and encourage formalization.

Government support is evolving to work hand-in-hand with fintechs, not just banks.

The fastest-growing segment in 2025, designed for speed, tech-integration, and flexible repayment models.

Each of these financing types comes with its own trade-offs. Choosing the right one depends on whether you value speed, cost, ownership, or risk distribution. The real question is ahead of you.

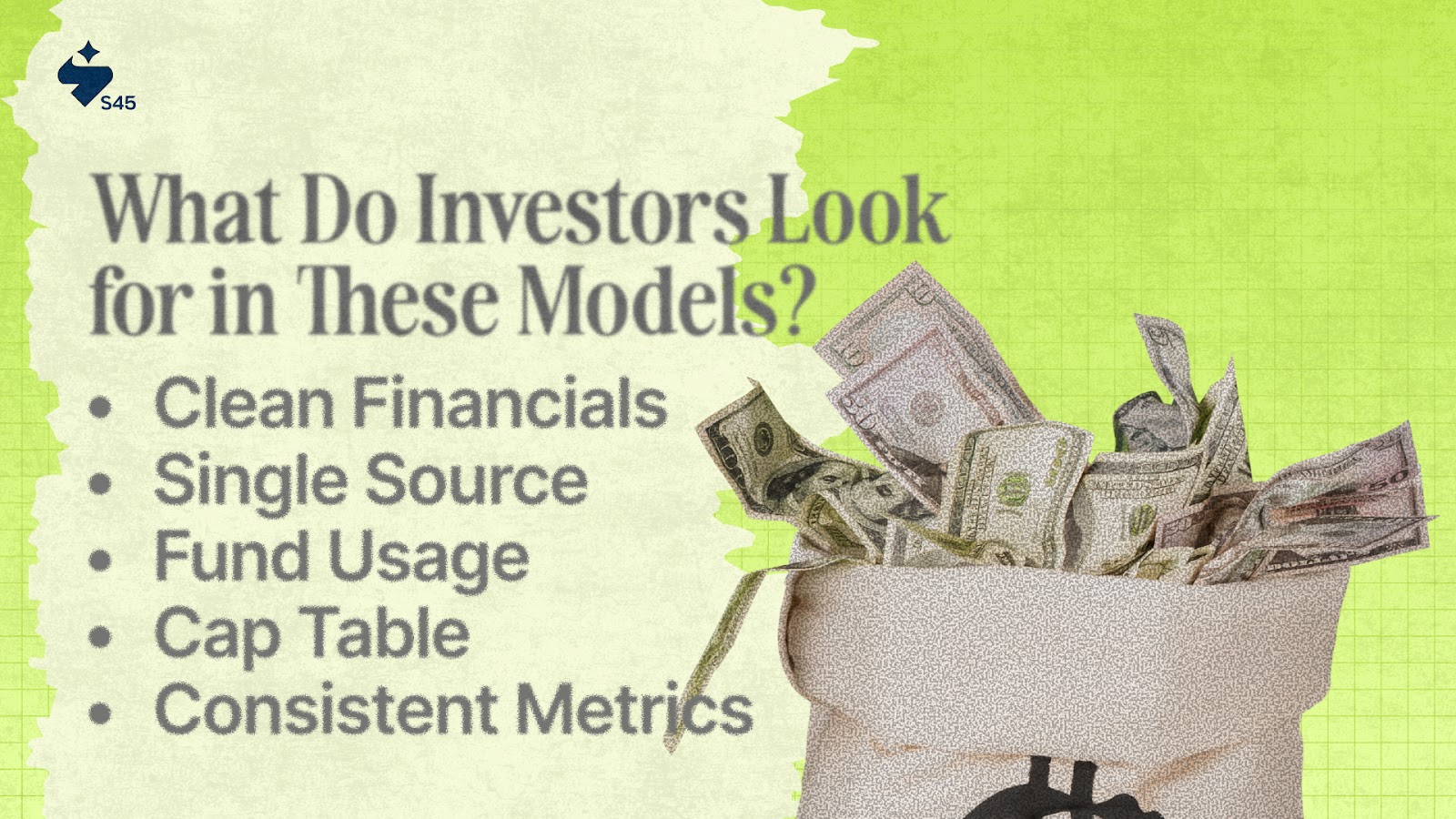

Each model has its own mechanics, but across the board, investors and platforms are scanning for one thing: clarity and consistency. Whether you’re approaching a revenue-based financing platform, a venture debt firm, or applying for a grant, your internal readiness signals how reliable your business is.

Here’s what they watch for beyond the pitch:

What do founders often overlook?

You’ve seen the models. Now it comes down to choosing the structure that actually fits how your business runs.

Founders often fixate on the source of the money. But the smarter question is: what kind of money serves your stage, risk appetite, and control preferences best?

Here’s how to think it through.

Choose equity (or equity-linked tools like SAFEs or convertible notes) when:

Equity is patient, but expensive. You’re not paying it back, but you're giving up a piece of everything you’ll build.

Debt-based models like RBF, venture debt, or invoice financing make sense when:

Debt is non-dilutive, but demanding. You keep control, but the repayments start soon, whether or not growth plays out as planned.

A blended approach works well when:

Hybrid models give you flexibility, but only if you manage complexity. The key is clean documentation, synced timelines, and clear communication with all stakeholders.

Exploring models such as revenue-based financing, venture debt, and invoice discounting helps you approach fundraising with greater clarity and intention. While these options open up smarter ways to fund your journey, choosing the wrong model or jumping in without a long-term view can lead to avoidable dilution, repayment strain, or stalled momentum.

If you're planning your next raise with a longer horizon in mind, S45club can help you structure smarter capital decisions, align funding with strategy, and stay in control of what you're building.

A. Always think a few steps ahead. Some founders accept capital that comes with restrictive terms, like aggressive repayment clauses or investor control rights, which complicate future fundraising. When choosing any model under SME alternative financing, make sure it aligns with your long-term roadmap and doesn’t scare off future VCs or institutional investors.

A. Yes, and many founders do it. For example, a startup might raise part of its capital via revenue-based financing to fund growth campaigns and use a small SAFE note for added runway. Just ensure your documentation is clean, terms are consistent, and future investors aren’t confused or put off by a complex structure. Always loop in legal advisors when mixing instruments.

A. Transparency is key. Your team should understand how any funding decision affects dilution, control, and company value. If you’re using SME alternative financing like venture debt or invoice discounting, walk them through how it preserves equity while fueling growth. This helps manage expectations, especially when negotiating ESOPs or performance-linked compensation.

A. Yes, though options may vary. Some models, like venture debt, often require you to have raised from a known VC. But others, like revenue-based financing, invoice discounting, or crowdfunding, are open to bootstrapped or angel-backed founders. SME alternative financing today is more inclusive than before, as long as your business metrics are healthy and well-documented.

A. Simplify your stack. Choose one model that fits your most immediate use case, say, RBF for performance marketing, and set up basic reporting templates to stay on top of repayments or investor communication. As your ops grow, you can layer in other tools. The key is to scale your financing model at the same pace as your internal systems.

Discover more insights on similar topics

Get startup insights and connect with our community