September 25, 202511 min read

Equity Advisor Duties: A Simple Guide for Indian Founders

By Abhishek Bhanushali

Finance Advice

Ever spent weeks preparing loan applications, only to face endless paperwork, repeated rejections, or vague responses from lenders? For many MSME founders, this isn’t an exception; it’s the norm.

In India, where MSMEs contribute nearly 30% of GDP and employ over 110 million people, limited access to credit remains one of the biggest obstacles. The challenges in accessing credit go beyond delays or paperwork. They trigger a domino effect across the business ecosystem.

When payroll is delayed, skilled workers migrate to competitors offering stability. Missed supplier payments result in withheld raw materials, leading to production stoppages that harm client relationships.

Additionally, a single rejected loan application can push founders towards high-cost informal borrowing at 24–36% interest, trapping them in a debt cycle. Worse, a lack of timely credit often means MSMEs cannot bid for large corporate or government contracts that require upfront capital.

The good news is that by understanding where the bottlenecks lie and what solutions are emerging, you can find more innovative ways to secure the financial backing your business needs.

Disclaimer: The information shared here is for general awareness about MSME credit challenges and solutions. It does not constitute financial advice. Please feel free to consult banks, fintech lenders, or certified financial advisors before making borrowing or investment decisions.

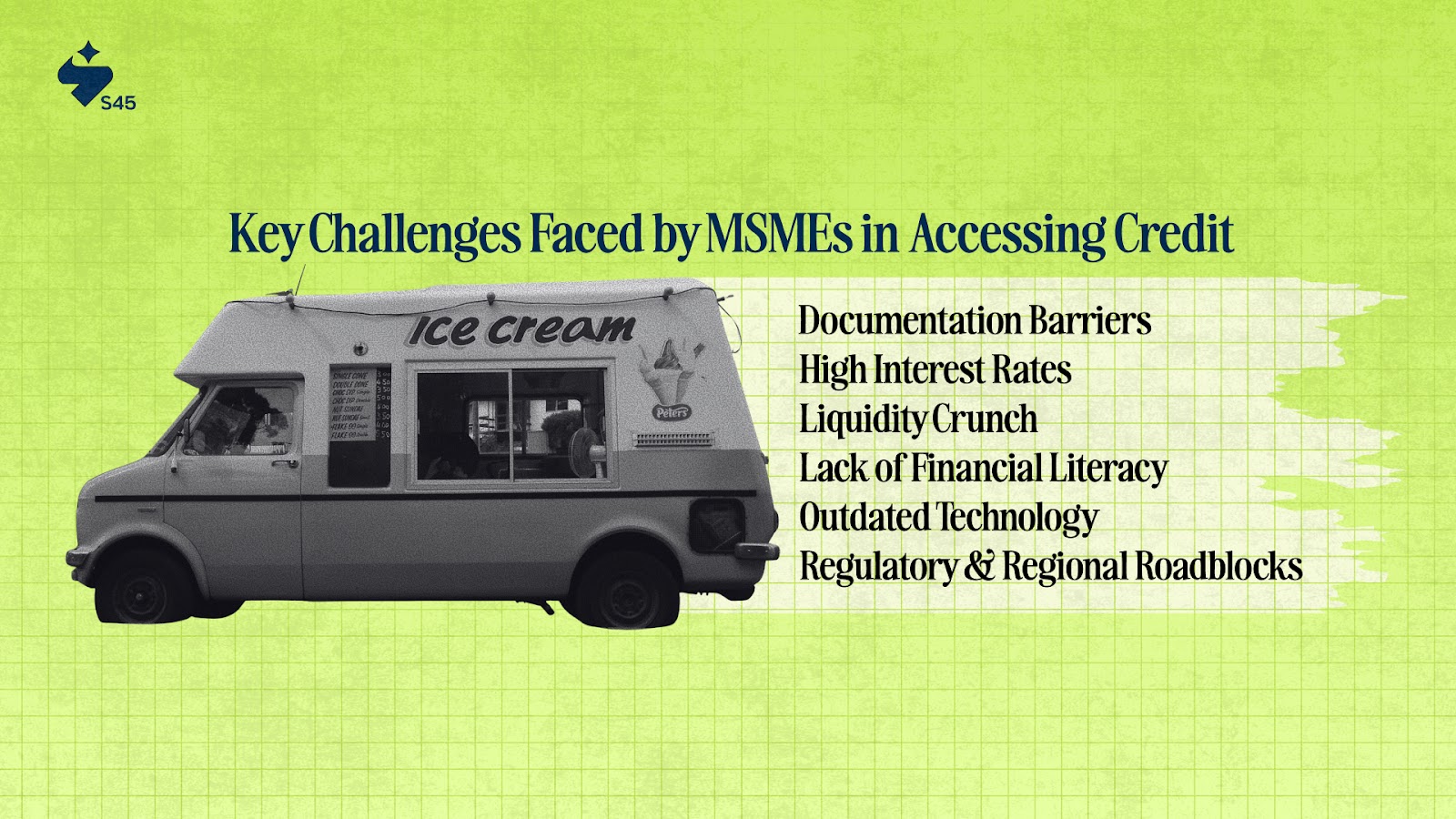

For many Indian MSMEs, securing credit feels like climbing a mountain with no clear path. The challenges faced by MSMEs in accessing credit directly impact their survival, expansion, and ability to compete with larger players. Here’s a closer look at what stands in the way.

Banks typically view MSMEs as high-risk borrowers, demanding collateral and lengthy documentation.

Example: A first-generation entrepreneur in Kanpur may run a successful textile unit but fail to secure a loan simply because he cannot pledge property as collateral.

By connecting founders to networks of alternative lenders and fintech platforms, S45 helps bridge the gap when banks hesitate.

Loans may get approved, but the terms often kill profitability.

Why it matters: A growing order book or solid business idea means little if the cost of credit eats away at margins before growth can take off.

Cash flow, not revenue, determines survival.

Pro Tip: Consider exploring invoice discounting and receivables exchanges to free up working capital more quickly.

Many entrepreneurs are masters of their craft but lack financial know-how. These include the following:

This is where platforms like S45 help by curating workshops and peer-sharing forums. Founders learn directly from business owners who’ve navigated the credit maze, making funding decisions more informed and less risky.

Where s45club fits: By curating workshops and peer-sharing forums, S45 enables founders to learn from experienced business owners who’ve navigated the credit maze.

Banks favor businesses with strong, digital records. Unfortunately, many MSMEs still operate informally.

Founder Impact: Informal systems may save costs in the short run, but they become expensive when your business is deemed “unfundable” at scale.

Did you know? As of August 2025, over 4 crore MSMEs are registered on the Udyam portal, a step that improves credit access, yet millions still operate outside the formal system.

Rules and geography decide credit access more than business potential.

Fintech lenders and NBFCs are beginning to bridge this gap with faster onboarding, digital-first approvals, and products tailored for underbanked regions. But awareness remains low among many MSMEs.

While these roadblocks can be discouraging, the financing landscape for MSMEs is undergoing rapid change. From digital lending to revenue-based financing, new-age solutions are making credit more accessible, and founders now have more options than ever.

The financing landscape in India is changing, and MSMEs no longer need to rely only on traditional banks. Here are some emerging solutions that can ease access to credit:

Invoice discounting allows you to unlock cash that is stuck in unpaid receivables.

Pro Tip: Use invoice discounting selectively for big-ticket buyers with reliable payment records; it reduces risk and lowers discounting fees.

Revenue-based financing lets you pay as you earn, rather than through fixed EMIs. Instead of rigid monthly repayments, you return a percentage of your revenue, which rises or falls with your sales.

P2P platforms directly connect lenders and borrowers, reducing the need for banks.

Pro Tip: Check platform credibility and repayment terms minutely.

Digital lending platforms provide paperless credit.

Pro Tip: Use digital lending for speed and short-term liquidity, but pair it with better record-keeping for long-term bank financing access.

This model lets you capitalize on your buyer’s credit strength instead of your own.

Beyond mainstream loans, MSMEs are embracing merchant cash advances. Here’s how it works:

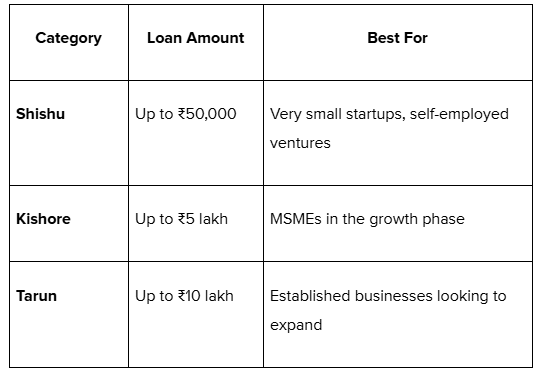

PMMY offers collateral-free loans tailored to business size and growth stage:

Impact: These loans serve as a stepping stone into the formal credit system.

Did you know? PMMY loans are designed to promote inclusivity, with special access for women, SC/ST, and OBC entrepreneurs.

With numerous financing options emerging, the real question for founders is not whether credit is available, but which option best suits their business. That’s where the proper guidance makes all the difference.

For many MSME founders, access to credit isn’t about a lack of ambition; it’s more about facing collateral demands, high interest rates, and confusing eligibility criteria. This is where S45 steps in as a growth partner, not just as another financing network.

Here’s how S45 supports you in solving credit hurdles:

For MSMEs, credit serves as a bridge to expansion, innovation, and long-term sustainability. Yet many founders remain locked out by outdated processes, collateral demands, and delayed payments.

The rise of fintech lending, supply chain finance, and government-backed schemes means access is improving. However, the real advantage lies in knowing which option fits your stage and strategy.

For too many MSMEs, funding delays mean missed opportunities, but it doesn’t have to be that way. At S45, we help founders overcome credit hurdles, discover more effective financing options, and enhance their credibility with lenders.

Connect with us today to turn credit access into your growth advantage.

MSME loans enable small and medium-sized businesses to expand, adopt new technologies, and access new markets. They create large-scale employment, strengthen rural and urban economies, contribute around 30% to India’s GDP, and promote inclusive, long-term national development.

Announced in Budget 2024-25, PSBs will use MSMEs’ digital footprints, including GST returns, utility bills, and online transactions, for in-house credit scoring. This reduces reliance on collateral, enables quicker approvals, lowers evaluation costs, and improves access for businesses with thin credit histories.

Pay your EMIs and dues on time, keep your credit utilization below 30%, and avoid making frequent loan applications. Regularly check your credit report for errors, build a mix of secured and unsecured loans, and maintain stable revenue to boost credibility with lenders.

The CGTMSE, established by the MSME Ministry and SIDBI, offers collateral-free credit to micro and small enterprises. By guaranteeing loans, it encourages banks to lend confidently, helping MSMEs access institutional credit for growth without needing property or heavy security.

AI and machine learning enable faster, more accurate credit assessments, reducing errors and bias. Blockchain boosts transparency, security, and fraud prevention in loan processes. Together, these technologies simplify access, cut delays, and make financing more reliable for MSMEs across India.

Discover more insights on similar topics

Get startup insights and connect with our community