September 25, 202510 min read

Debt-to-Asset Ratio: Calculation & Importance Explained

By Abhishek Bhanushali

Debt & Equity Financing

Looking to raise capital without giving away equity right away?

Many Indian startups and SMEs are using Compulsory Convertible Debentures (CCDs) to fund early growth while delaying valuation decisions. CCDs offer structured funding without immediate dilution, making them an attractive option for founders and investors.

In 2022, the Indian government extended the conversion timeline for CCDs from 5 to 10 years, but this applies specifically to DPIIT-recognized startups, giving qualifying businesses more room to grow before equity conversion. This shift adds flexibility for founders to strengthen operations before bringing in shareholders.

At the same time, investors gain better visibility into a company’s performance before converting their debt into equity. When used thoughtfully, CCDs strike a balance between growth capital and long-term ownership planning.

In this guide, you’ll learn how CCDs work in practice, how they compare to other options, the key legal and tax aspects, and when they fit best into your funding strategy.

Compulsory Convertible Debentures (CCDs) are debt instruments that must convert into equity after a fixed period or on a specific event. The terms of conversion, including timing and share ratio, are pre-agreed between the investor and the company. Unlike regular debt, CCDs are not repaid in cash; they turn into shares.

CCDs sit between debt and equity. They offer capital today while postponing dilution until later. Many early-stage and growth-stage companies in India prefer CCDs for this reason. The investor earns interest during the holding period, and the company benefits from delayed equity dilution.

CCDs mean raising money with a clear equity outcome later. Understanding their features helps you know if they fit your funding plan.

CCDs come with a fixed structure, making them different from traditional debt or equity. They’re not open-ended or negotiable over time. Both the investor and the company know how and when the CCDs will convert into shares. This clarity makes CCDs useful for structured funding.

Let’s look at the main features that define CCDs.

Each feature plays a clear role in how CCDs function as a funding tool. Understanding how they work in practice gives you better clarity on when to use them.

CCDs follow a fixed structure. A company issues them to investors with clear terms for interest, tenure, and conversion. They’re registered as debt instruments first, and later convert into equity when the agreed conditions are met. This allows founders to raise money without giving up shares immediately.

Here’s how CCDs typically work in Indian startups and SMEs:

This system works best when both sides agree on the long-term vision. Knowing why startups and SMEs choose CCDs helps you understand where they fit into a growth plan.

Raising capital is always a balancing act, especially in the early stages of a business. Founders often want to delay dilution, while investors seek security and upside. Compulsory Convertible Debentures (CCDs) offer a middle ground. They work well when the business needs capital but isn't ready to price its equity yet.

Here’s why CCDs are popular among startups and SMEs:

In addition to that, platforms like S45 further simplify the process by standardizing deal structures, making it easier for SMEs to stay investor-ready.

CCDs are often seen as startup-friendly convertible instruments in India. Before using them, it’s important to understand the rules that govern them.

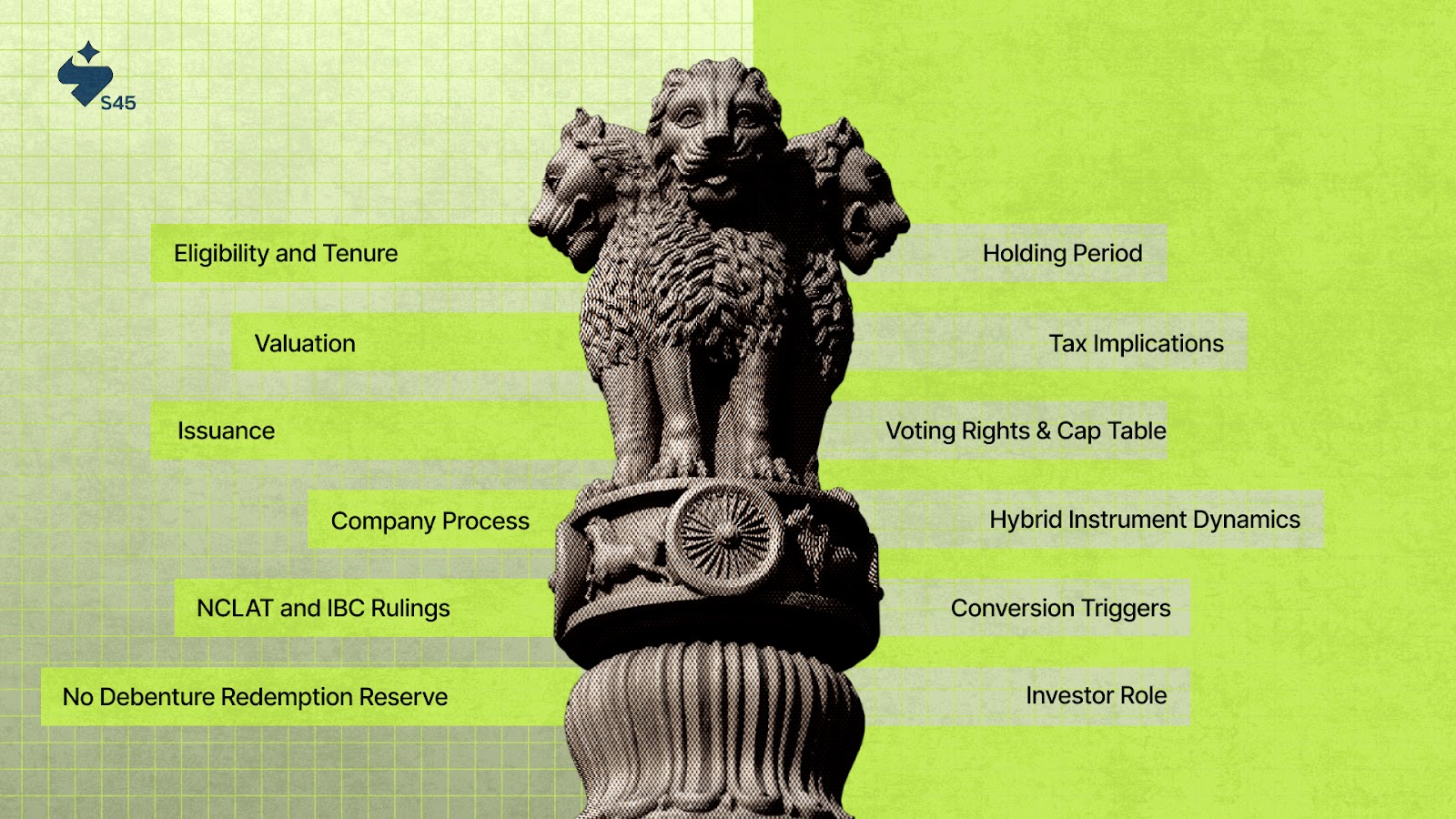

Compulsory Convertible Debentures (CCDs) are hybrid instruments that occupy a unique space in Indian corporate funding. Their classification as debt, equity, or a mix is shaped by several laws and regulatory bodies.

Understanding the legal and compliance landscape of CCDs is important for companies, founders, and investors to avoid regulatory pitfalls, enable smooth issuance and conversion, and optimize tax treatment.

Each of these legal regimes views CCDs differently, requiring synchronized compliance at every stage, from structuring, issuance, and accounting to conversion and exit. Let’s have a look at various aspects:

CCDs are classified as debentures, meaning instruments of company indebtedness. Issuing CCDs requires:

Fully and compulsorily convertible debentures are exempt from maintaining a Debenture Redemption Reserve. Conversion terms (tenure, interest, conversion ratio) must be specified upfront and cannot be varied easily.

CCDs are shown as liabilities (“borrowings”) in the balance sheet until they convert. After conversion, they move to equity, reflecting the shift from creditor to shareholder.

The Supreme Court in Narendra Kumar Maheshwari v. Union of India clarified that compulsory conversion distinguishes CCDs from classic debt; they are treated as equity instruments for capital market regulations, since there's no repayment of principal.

Regulatory agencies like SEBI consider CCDs as equity from the outset when their conversion is mandatory and predetermined.

Under Section 5(8)(c) of IBC, debentures are prima facie ‘financial debt’ since they are money raised for time value. However, if a CCD’s terms specify only conversion (with no principal repayment), recent judicial and NCLAT pronouncements have argued they function more like equity, denying creditor rights at the insolvency stage.

The Supreme Court's ruling in IFCI Ltd. v. Sutanu Sinha and ensuing NCLAT judgments underscore that final classification in insolvency depends on the instrument’s precise contractual terms and how it is reflected in the financial statements.

FEMA and its 2017 regulations treat CCDs held by non-residents as 'capital instruments,' making them similar to equity from a cross-border FDI perspective.

Key requirements include:

Interest paid on CCDs before conversion qualifies as a tax-deductible business expense under Section 36(1)(iii) of the Income Tax Act, provided the CCDs are issued for business purposes.

Multiple judicial decisions (such as the Bangalore Tribunal in CAE Flight Training (India) (P) Ltd.) confirm that interest continues to be treated as debt expense until the date of conversion.

Costs incurred for issuing CCDs, such as legal or placement fees, can generally be amortized or allowed as a deduction, per precedents set by courts, including in Ashima Syntex v. Asstt. CIT and CIT v. Secure Meters Ltd.

The act of conversion is not usually treated as a taxable transfer event. However, Section 56(2)(viib) scrutiny applies if shares are issued at a premium, so robust valuation is critical during both issuance and conversion.

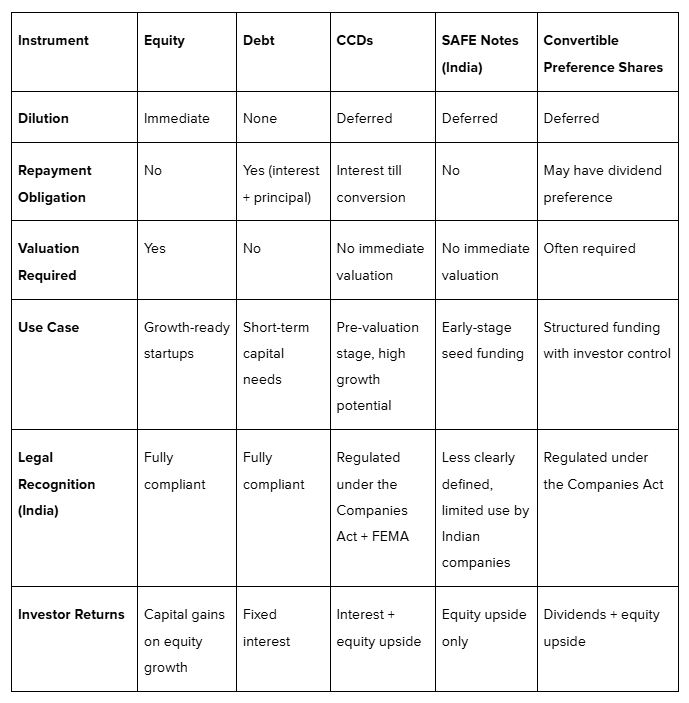

From a compliance perspective, CCDs demand rigorous attention to their hybrid character, balancing debt-like protections and equity, like obligations across regulatory regimes. This multi-dimensional legal profile is vital when comparing CCDs to pure equity instruments, classic debt, or alternatives like SAFE notes or convertible notes.

Startups have several options to raise money; each comes with its own pros, risks, and use cases. While CCDs offer a flexible way to raise funds, they’re not the only option. Understanding how CCDs compare with equity, debt, and other instruments like SAFE notes helps you pick the right tool at the right stage.

Here’s a quick comparison to make that decision easier:

CCDs balance the flexibility of equity with the safety of debt, making them ideal for early growth phases. But they’re not always the best fit; choosing the right tool depends on the stage, needs, and clarity of your business plan.

CCDs can help raise funds without giving up control right away. However, they also come with trade-offs that founders must be aware of. The structure is hybrid; it initially behaves like debt and later converts into equity. If you’re not prepared, CCDs can create confusion, legal risk, and long-term dilution.

Let’s examine common risks and learn how to manage them effectively.

Though CCDs are flexible, they demand a strong understanding of terms, ownership, and investor relations. Used wisely, these risks can be managed and turned into growth opportunities.

Issuing Compulsorily Convertible Debentures (CCDs) involves a structured approach to ensure regulatory compliance and smooth processing. The process balances legal formalities, shareholder approvals, and operational steps, each essential to successful issuance and future conversion.

Understanding and following these steps minimizes delays and legal risks, helping companies raise capital efficiently.

The procedure can be broken down into clear sequential steps:

The company convenes a board meeting to approve the issuance of CCDs, including deciding the investors, issue size, interest rate, conversion terms, and tenure. This formal approval ensures that the company’s key decision-makers agree to the deal’s framework and terms. To avoid ambiguities, keep detailed records of resolutions and terms decided at this stage.

The company drafts a detailed agreement outlining key terms such as conversion ratio, triggering events, interest rate, and rights of the investors. The term sheet summarizes these key points. Clarity here prevents future disputes and aligns expectations. Seeking legal counsel for precise drafting helps mitigate risks of ambiguous or incomplete terms.

A valuation by a registered valuer (for domestic investors) or a chartered accountant (for foreign investors) is necessary to fix the conversion price or formula, complying with tax and FEMA regulations. Getting this report early ensures compliance and smooth pricing negotiations. Delays can be minimized by selecting experienced valuers familiar with startup valuations.

A separate bank account must be opened specifically for receiving subscription money from CCD investors. It ensures transparency and regulatory compliance concerning fund flows. Maintaining this account until conversion avoids commingling and audit issues.

An Extraordinary General Meeting (EGM) is called to obtain shareholder approval via a special resolution for CCD issuance. Proper advance notice and adherence to quorum requirements prevent procedural irregularities. This step is crucial, as failing to secure shareholders’ consent can invalidate the issuance.

After shareholder approval, the company files Form MGT-14 (for special resolution), PAS-4 (offer letter), PAS-3 (allotment details), and PAS-5 (annual return of allotments) with the RoC. Timely and accurate filings avoid penalties and regulatory scrutiny. Employing company secretarial professionals ensures this compliance is met seamlessly.

The company sends formal offer letters to investors with details and collects subscription money. Upon receipt, CCD allotment certificates are issued. Proper documentation and stamping of certificates are essential to establish investor rights and validate investments.

If CCDs are issued to foreign investors, obtain KYC and Foreign Inward Remittance Certificates (FIRC), and file the FC-GPR form with the Reserve Bank of India (RBI) to comply with FEMA rules. Missing or delayed filings here can lead to penalties or restrictions on future repatriation.

Adhering to these steps, companies can ensure regulatory approval and operational readiness for CCD issuance. Proper legal and procedural discipline at each stage prevents delays that could risk the capital raise or conversion process.

Understanding these steps with care is important to using CCDs effectively as a funding tool and preparing for future conversion into equity. Now, let’s see how S45 can help SMEs eyeing CCDs.

S45 is a growth partner for Indian SMEs with ₹100 Cr+ in revenue and ₹10 Cr+ in annual profit. It helps founder-led businesses scale with better capital access, governance systems, and strategic clarity. If you're considering CCDs or hybrid instruments, S45 brings the right expertise and network to the table.

Here’s how S45 supports CCD-ready founders:

S45 makes CCD planning easier, safer, and more founder-friendly. It’s not just support; it’s shared experience. Plan your next raise confidently with S45’s expert team and founder-first approach.

Compulsory Convertible Debentures (CCDs) are a smart funding option for high-growth firms that need capital now but want to delay equity dilution. They combine the safety of debt with the upside of equity, making them ideal for early-stage companies or profitable SMEs planning structured expansion.

But CCDs aren't plug-and-play; they require sound legal drafting, compliance with Indian laws, and clarity on terms like conversion timelines, interest rates, and investor rights.

When used without guidance, they can cause dilution shocks or control issues. But with the right usage, they help build a financial map and delay valuation talks until the business is stronger. CCDs work best for firms confident in growth but not ready for traditional equity.

Is your next fundraising structured for long-term success or just a short-term patch? Book a free demo to speak with the experts at S45 to use CCDs wisely and plan legally and financially for long-term growth.

CCDs are treated as debt at the time of issuance. They convert into equity after a fixed period or event. Until conversion, they follow debt rules, including interest payment and compliance under the Companies Act and RBI regulations.

Yes, foreign investors can invest in CCDs under the automatic route if pricing, valuation, and conversion terms follow RBI guidelines and FEMA rules. Legal vetting and regulatory compliance are essential in such cases.

Interest earned on CCDs before conversion is taxable as income. After conversion, capital gains tax may apply based on the holding period of the resulting equity shares. Firms must consult tax experts to plan better.

Yes, a valuation report from a registered valuer is usually required to fix the conversion price of CCDs. It helps in meeting regulatory requirements and avoiding future disputes with investors or tax authorities.

There’s no fixed minimum tenure under the Companies Act, but for foreign investors, RBI guidelines mandate a minimum maturity of one year. Most CCDs convert within 3–5 years, depending on growth plans and deal terms.

Discover more insights on similar topics

Get startup insights and connect with our community